Pakistan’s Circular Debt Hits 4% of GDP Despite Reforms

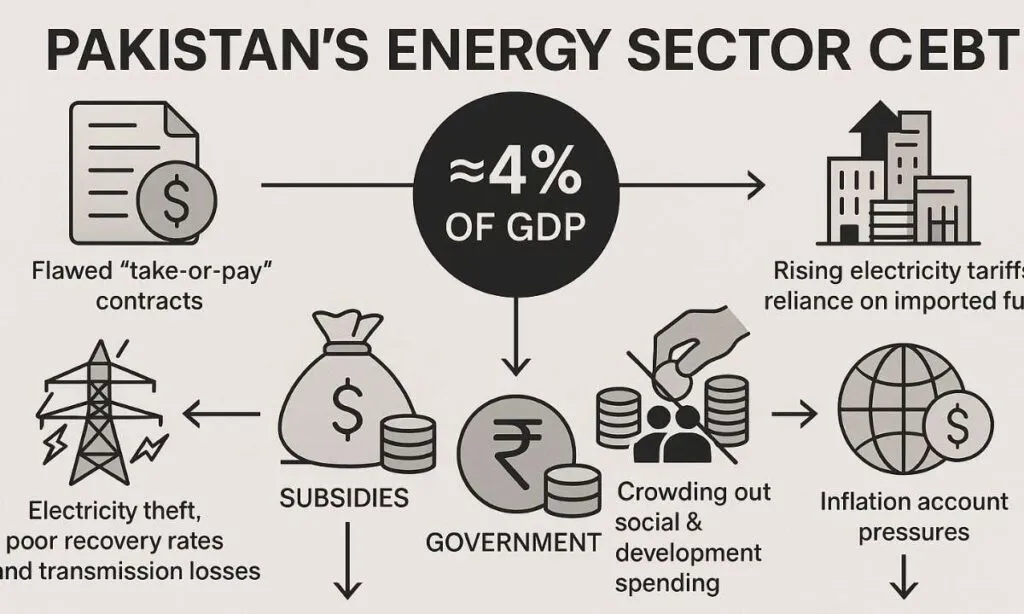

Circular debt in Pakistan’s energy sector has surged to nearly 4% of GDP, underscoring the lack of structural reform and deepening fiscal, inflationary, and external pressures.

Pakistan’s circular debt problem has become a defining feature of its economic challenges, symbolizing the country’s failure to implement long-promised structural reforms.

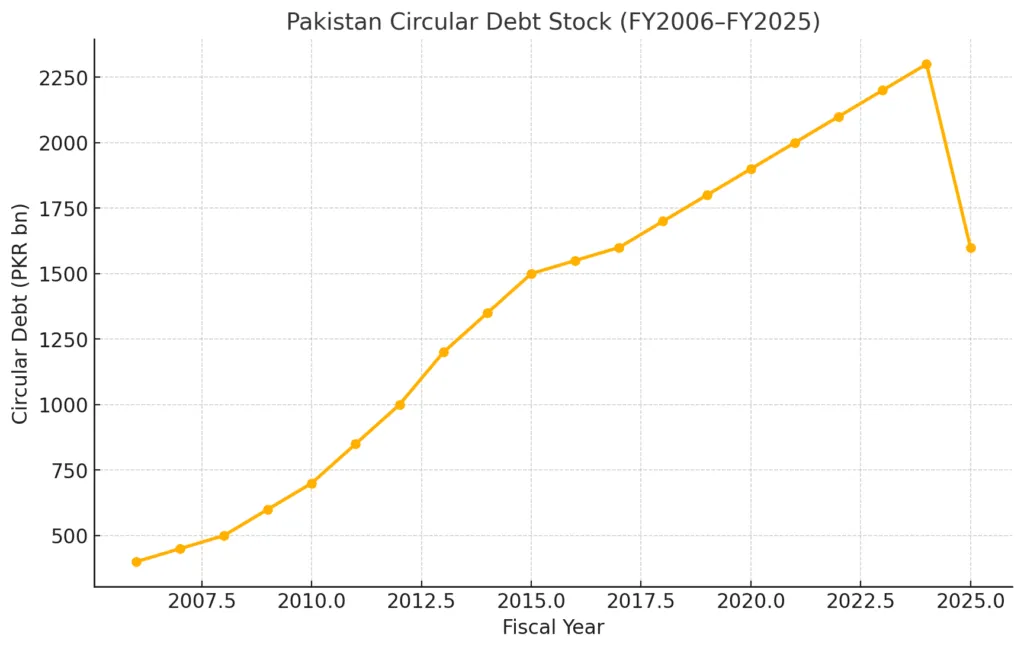

Despite repeated attempts at reform and periodic payments to reduce the debt stock, circular debt in the energy sector has continued to rise, standing at PKR 1.6 trillion (1.4% of GDP) as of June 2025. This figure is compounded by an additional PKR 3 trillion (2.6% of GDP) owed by electricity producers to oil and gas suppliers, bringing the total to around 4% of GDP.

Key Takeaways

- Pakistan’s circular debt in the energy sector has reached about 4% of GDP, despite repeated bailouts and reforms.

- Flawed “take-or-pay” contracts, electricity theft, poor recovery rates, and transmission losses remain core drivers.

- The government’s subsidies and PHL debt absorption have strained fiscal space, crowding out social and development spending.

- Rising electricity tariffs and reliance on imported fuel continue to fuel inflation and external account pressures.

- Partial reforms such as renegotiated contracts and CTBCM introduction have slowed, but not stopped, debt accumulation.

According to a study, the circular debt issue is not new. Since its emergence in 2006, it has repeatedly been flagged by policymakers, economists, and international lenders as one of Pakistan’s most critical structural bottlenecks. Yet the debt has only grown larger, with successive governments failing to implement the difficult reforms needed to address its root causes.PSX Surges on Circular Debt Breakthrough

A recent PKR 0.8 trillion clearance offered temporary relief but did little to stop the accumulation of new arrears. The problem now reverberates throughout Pakistan’s economy, affecting fiscal sustainability, inflation, external accounts, growth, and financial stability.

At its core, circular debt is the accumulation of unpaid bills throughout the electricity supply chain. The process begins when distribution companies (DISCOs) fail to collect payments from consumers, often due to electricity theft, weak billing efficiency, or deliberate non-payment by government entities.

This shortfall means that DISCOs cannot fully pay the Central Power Purchasing Agency (CPPA-G), which acts as the market operator. CPPA-G then defaults on payments to the National Transmission and Dispatch Company (NTDC) and energy producers. Finally, independent power producers (IPPs) and public generation companies fall behind on their payments to fuel suppliers, mainly oil and gas companies. This cycle perpetuates debt accumulation, keeping the sector locked in financial stress.

Structural Flaws

One of the most significant structural flaws lies in the contractual framework with IPPs. For years, the government has relied on “take-or-pay” agreements, which obligate it to purchase 100% of a power producer’s installed capacity regardless of actual demand. While these contracts were originally designed to attract private investment into the power sector, they have now created a costly mismatch.

By FY2023/24, Pakistan’s installed capacity stood at 46 gigawatts, while average demand utilization was only 15.5 gigawatts. This meant consumers were paying for nearly 30 gigawatts of idle capacity throughout the year. Adding to the financial strain, these contracts are indexed in US dollars, which has significantly increased payment obligations during periods of rupee depreciation.

Chronic Losses

Transmission and distribution (T&D) losses are another chronic weakness. Despite having an energy surplus on paper, outdated grid infrastructure and poor investment prevent efficient power transmission. Grid constraints, inadequate maintenance, and weak connectivity between southern production hubs and central demand centers frequently result in unmet demand.

Moreover, three DISCOs cover about 62% of Pakistan’s territory, creating operational imbalances and inefficiencies. T&D losses combined with low recovery rates consistently undermine revenue flows.

Tariff Strucutre

The tariff structure also contributes to circular debt. The National Electric Power Regulatory Authority (NEPRA) sets tariffs based on cost recovery assumptions, but these assumptions often prove unrealistic. Recovery rates are typically far below 100%, and T&D losses exceed projected levels.

Compounding this problem, government-notified tariffs are often set below NEPRA’s recommendations to keep electricity affordable for consumers. To cover the gap, the government promises tariff differential subsidies. However, these subsidies are frequently underfunded or delayed, leaving DISCOs with further shortfalls. The result is a recurring cycle of arrears that keeps circular debt growing.

Political Interference

Governance weaknesses in the energy sector remain a persistent drag. Political interference in DISCO operations, lack of accountability, and entrenched mismanagement have made reforms difficult. Most DISCOs fail to meet NEPRA’s recovery and T&D targets.

The system of uniform tariffs, which forces efficient DISCOs to subsidize inefficient ones through surcharges, further removes incentives for improvement. Cross-subsidization, rather than performance-driven accountability, has left the sector in a state of inertia.

The impact of circular debt on Pakistan’s fiscal position has been significant. To manage the rising costs, the government created Power Holding Limited (PHL), a special vehicle tasked with holding and servicing power sector debt. However, PHL was eventually absorbed into the government’s own debt profile, raising public debt and exposing the sovereign to greater risk.

At present, circular debt accounts for about 2.2% of total government debt, excluding direct obligations of public sector generation companies to fuel suppliers. Energy subsidies and debt servicing continue to exert pressure on fiscal balances, diverting resources away from infrastructure development, education, and health programs.

Heavy Reliance on Domestic Banks

The financial sector has also been affected. Heavy reliance on domestic banks to fund PHL debt has contributed to the crowding out of private credit, constraining investment and growth in other parts of the economy.

Meanwhile, persistent load-shedding, often used as a penalty in areas with low collection rates, disrupts industrial output, particularly in manufacturing. Businesses face higher operating costs and reduced productivity, while frequent outages undermine investor confidence.

Inflationary pressures have been amplified by rising electricity tariffs, which feed into broader consumer prices. Imported fuel dependency worsens Pakistan’s external balance, especially during episodes of sharp rupee depreciation.

The combination of high energy costs and currency volatility has deepened external vulnerabilities, placing additional pressure on foreign exchange reserves.

Reforms

In recent years, authorities have launched a series of reforms aimed at breaking the cycle. The introduction of the Competitive Trading Bilateral Contract Market (CTBCM) is intended to dismantle DISCO monopolies by allowing large consumers to purchase electricity directly from producers.

Renegotiation of IPP contracts has shifted some agreements from “take-or-pay” to “take-and-pay,” where payments are made only for consumed energy. Tariff hikes and more targeted subsidies have been rolled out to reduce fiscal strain. The government has also taken steps to reduce reliance on imported fuel by expanding domestic hydropower and coal capacity.

Additional initiatives include crackdowns on electricity theft, improvements in billing and collections, and infrastructure investments to reduce T&D losses. On paper, these represent meaningful steps toward reform. However, the persistence of circular debt suggests that progress remains insufficient. The structural flaws in governance and contract management continue to outpace the gains from reform measures.

The issue also remains politically sensitive. Successive governments have been reluctant to raise tariffs to cost-recovery levels, fearing public backlash and inflationary consequences. Meanwhile, entrenched interests within the energy sector have resisted reforms that threaten existing privileges. As a result, reforms have been partial, delayed, or reversed, preventing meaningful progress.

International financial institutions, including the International Monetary Fund (IMF), have repeatedly identified energy sector reform as a priority for Pakistan. During bailout negotiations, the IMF has pressed for reductions in circular debt, cost-reflective tariffs, and improved governance. While Pakistan has made commitments under IMF programs, implementation has often lagged once the immediate pressure eases.

Historically, Pakistan has oscillated between short-term fixes and partial reforms. For example, earlier efforts to pay down circular debt through one-off injections temporarily reduced arrears but failed to address structural drivers.

The result has been a recurring cycle of debt buildup, repayment, and re-accumulation. The current stock of circular debt, at roughly 4% of GDP, underscores how little progress has been made despite repeated interventions over nearly two decades.

The economic costs are increasingly unsustainable. Without comprehensive reform, circular debt will continue to absorb fiscal resources, weaken investor confidence, and constrain growth. Reducing arrears will require a multipronged approach: improving DISCO governance, depoliticizing tariff-setting, renegotiating legacy contracts, investing in grid infrastructure, and transitioning toward competitive markets. Only such structural measures can break the cycle of accumulation.

Until then, circular debt will remain one of Pakistan’s most intractable challenges. Its persistence not only reflects the inefficiencies of the energy sector but also illustrates the broader struggle of Pakistan’s economy to move beyond stopgap measures and embrace long-term reform.

Circular debt will continue to weigh on Pakistan’s economy until systemic inefficiencies in the energy sector are addressed, making it among the most urgent reforms needed for the country’s fiscal and economic future.Read More Stories on NewzToday