GDP grew 2.4% in 3QFY25

ISLAMABAD: Pakistan posted real GDP growth of 2.4% during 3QFY25 compared to revised estimates of 1.5% and 1.4% for 2QFY25 and 1QFY25, respectively. The average quarterly growth for 9MFY25 is estimated around 1.8%.

The 113th meeting of the National Accounts Committee (NAC) was held today in the N3C, Pakistan Bureau of Statistics, Headquarters, Statistics House, G-9/1, Islamabad. The Secretary, M/O PD&SI chaired the meeting. The committee approved the quarterly GDP growth rates for Q1 (Revised), Q2 (Revised), and Q3 during FY 2024-25 and annual growth rates for 2022-23 (Final), 2023-24 (Revised) and 2024-25 (Provisional).

The committee approved the revised first and second quarter estimates of 2024-25. Overall GDP for Q1 and Q2 for FY 2024-25 has witnessed a revised growth of 1.37% and 1.53% as compared to 1.34% and 1.73% estimated in 112th NAC meeting.

The updated growth rates in agriculture during Q1 is 0.84% as compared to 0.74% presented earlier.

NEPRA concerned over Disco’s inaccurate data

The upward revision in Q1 is due to improvement in other crops from 0.43% to 5.53% and forestry from -2.07% to 0.79%. While there is improvement in other crops from 0.73% to 5.52%, forestry from -0.64% to 3.18% and fishing from 0.79% to 1.63%, important crops in Q2 have further moved down from -7.65% to -12.09% causing downward revision in agriculture from 1.10% to 0.79%. Despite improvement in mining and quarrying from -8.06% to -6.25%, the industrial activities have posted downward revision from -0.66% to -0.91% due to decline in electricity, gas and water supply from +1.37 to -2.30% in the updated estimates for Q1.

The Q2 growth in industrial activities has witnessed downward revision from -0.18% to -0.99% mainly due to electricity, gas and water supply, which moved down to -3.40% as compared to 7.71% estimated earlier.

The revised growth in services during Q1 and Q2 has slightly improved from 2.21% and 2.57% to 2.28% and 2.59% respectively due to improvement in wholesale & retail trade, transportation & storage, information and communication, and public administration & social security.

The economy has posted a stable growth of 2.40% during Q3 of FY 2024-25. The growth in agriculture, industry and services stands at 1.18%, -1.14% and 3.99% respectively.

In agriculture, although important crops have declined by -11.14% but other crops have grown by 4.84% on account of double digit growth in production of onion (11%) and mango (26%). Livestock (4.42%), forestry (4.25%) and fishing (0.50%) have also registered positive growth rates during Q3 FY 2024- 25. The negative growth rate in industry (-1.14%) is due to mining & quarrying (-3.96%), large-scale manufacturing (-0.89%), electricity, gas and water supply (-7.72%) and construction (-9.12%).

The overall growth in services is 3.99% during Q3 2024-25 with all the constituents contributing positively i.e. wholesale & retail trade (+1.57%), transportation & storage (+0.67%), information and communication (+18.44%), finance & insurance activities (+10.65%), public administration and social security (+13.73%) education (+4.63%), health & social work (5.06%) and other private services (+2.93%).

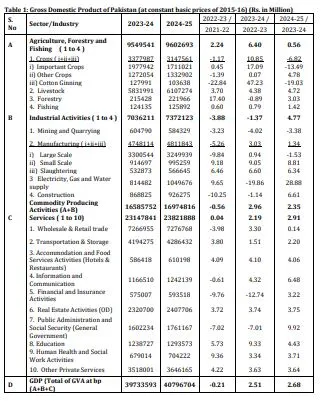

The committee approved the overall final growth of annual GDP during FY 2022-23 at -0.21%, which was estimated at -0.22% in the 111th meeting. The final growth rates in agriculture, industry and services during FY 2022-23 are 2.24%, -3.88% and 0.04% respectively. Further, the revised growth during FY 2023-24 is 2.51%, which was estimated at Page 2 of 3 2.50% in the previous meeting.

In the revised estimates, agriculture has improved from 6.18% to 6.40%, the industry has improved from -1.65% to -1.37%, whereas services have slightly declined from 2.35% to 2.19% due to downward revision in transportation & storage (from 2.12% to 1.51%) and human health & social work activities (from 5.99% to 3.34%) (Table 1).

The committee also approved the provisional growth of GDP at 2.68% during on-going FY 2024-25.

The provisional growth rates in agriculture, industry and services are 0.56%, 4.77% and 2.91% respectively. In agriculture, important crops have declined by 13.49% due to decrease in production of wheat (-8.91% from 31.81 to 28.98 MT), maize (-15.4% from 9.74 to 8.24 million tons), rice (-1.38% from 9.86 to 9.72 million Tons), sugarcane (-3.88% from 87.64 to 84.24 million tons) and cotton (-30.7% from 10.22 to 7.08 million bales). Despite reduction in the production of grams (-16.6%), other crops have posted a provisional growth of 4.78% due to double-digit growth in the production of potato (11.5% from 8.43 to 9.40 million tons), onion (15.9% from 2.30 to 2.67 million tons), mango (26.7% from 2.09 to 2.65 million tons), and sesame (44.7% from 0.30 to 0.44 million tons).

While cotton ginning & miscellaneous component has declined by 19.03%, livestock, forestry and fishing have posted provisional growth rates of 4.72%, 3.03% and 1.42% respectively (Table 1).

Industry in 2024-25, has shown a growth of 4.77% provisionally. Despite increase in the production of coal (2.84%), mining & quarrying industry has contracted by 3.38% because of decrease in production of natural gas (-7.05%), crude oil (-14.72%) and other minerals.

Large scale manufacturing, which is based on Quantum Index of Manufacturing (QIM) (July-March), has witnessed a negative growth of 1.53% with mixed trend in the production of various groups e.g. Food (-0.49%), Beverages (+0.88%), Tobacco (+13.12%), Textile (+2.15%), Wearing apparel (+7.62%), Coke & Petroleum (+4.48%), Chemicals (-5.51%), Non-metallic mineral products (-10.45%), Iron & steel products (-10.94%), Fabricated metal (-17.16%), Electrical equipment (-15.89%) and Automobiles (+40.0%). Electricity, gas and water supply industry has shown a positive growth of 28.88% primarily due to low base effect of FY 2023-24 i.e. -19.86% as well increase in output of WAPDA & companies. Construction industry increased by 6.61% due to increase in construction-related expenditures by the private sector and general government (Table 1).

Services industry has also shown a growth of 2.91% in 2024-25 with positive contributions from all the constituents.

Wholesale and retail trade has witnessed a modest growth of 0.14% because of slower output growth in agriculture and manufacturing.

Transport and storage industry has increased by 2.20% because of increase in output of water, air and road transport. Information & Communication has grown by 6.48% due to increase in output of computer programming and consultancy activities (24%).

Slower rate of inflation and low base effect has resulted into positive growth rates in Finance & Insurance and Public Administration and Social Security industries at 3.22% and 9.92% respectively. Further, both Education and Human health and Social Work industries have posted positive growth of 4.43% and 3.71% respectively. Other private services have been estimated at 3.64% on the basis of indicators received from the sources (Table 1)

On the basis of latest figures of the national accounts aggregates for FY 2024-25, the overall size of the economy stands at Rs.114.7 trillion i.e. US$ 410.96 billion as compared to Rs.105.1 trillion i.e. US$ 371.66 billion. Further, per capita income in Rupees is 509,174/- i.e. US$ 1824/-. However, the series of per capita income from 2016-17 onwards will be revised after the receipt of backward and forward projections of population from the sources on the basis of 2023- Population Census.

Overall the forum appreciated the efforts of National Accounts team of PBS and key stakeholders including Ministry of Planning Development and Special Initiatives, Ministry of Finance and State Bank of Pakistan in preparation of quarterly GDP and annual GDP.