Indus Motor FY25 results show 53% profit growth

Company announces Rs50/share final dividend, but earnings fall below industry expectations due to weaker margins

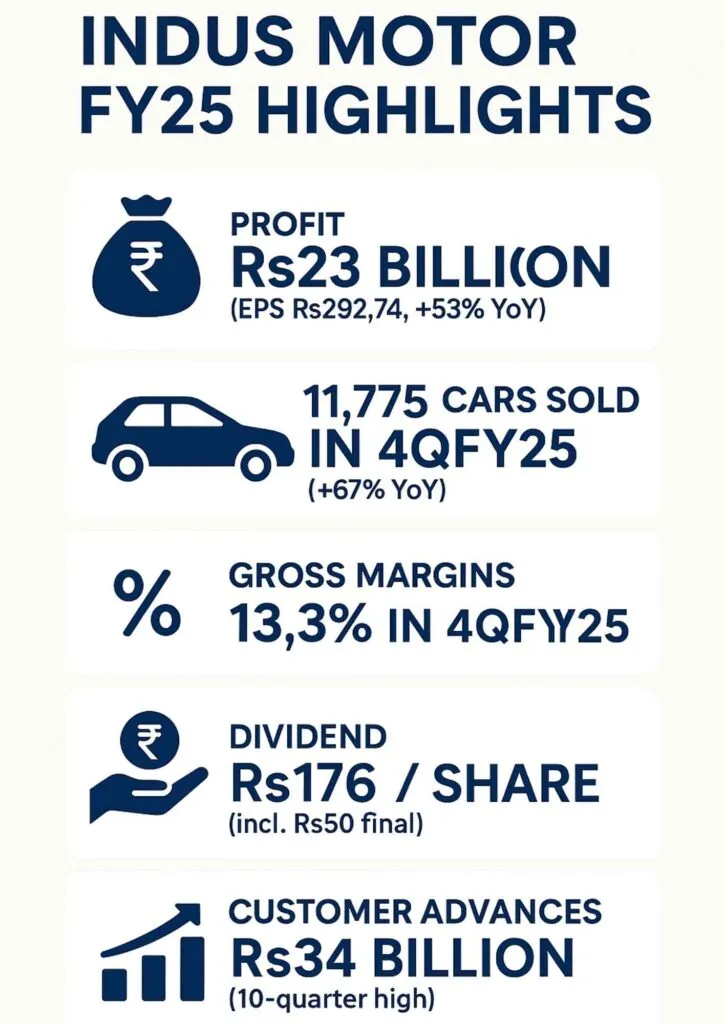

Indus Motor Company Limited (INDU) has posted a net profit of Rs23 billion for the fiscal year ended June 30, 2025, translating into earnings per share (EPS) of Rs292.74, up 53% year-on-year from Rs191.10 in FY24. The results, announced on August 29, 2025, were below market expectations as gross margins slipped in the final quarter.Car sales up 39% in 11MFY25

During the fourth quarter of FY25, the automaker reported earnings of Rs6.4 billion, or EPS of Rs81.88, compared with Rs5.7 billion, or EPS of Rs72.08, in the same period last year. This reflected a 14% annual increase but a 2% sequential decline compared to the preceding quarter. Analysts attributed the shortfall relative to consensus forecasts to lower-than-expected gross margins.

Gross margins for 4QFY25 stood at 13.3%, down from 14.2% in 4QFY24 and 16.9% in 3QFY25. The decline was linked to a sales mix skewed more toward Corolla, Yaris, and Corolla Cross models, which generally carry lower margins, compared to higher-margin Fortuner and Hilux models. Analysts also pointed to intensified competition from newly introduced Chinese pickups and SUVs, which likely ate into sales of INDU’s flagship Fortuner and Hilux vehicles. On a full-year basis, however, gross margins improved to 14.5% from 12.7% in FY24, suggesting stronger operational efficiency across the year despite the quarterly dip.

The company’s Board of Directors announced a final cash dividend of Rs50 per share, bringing the total payout for FY25 to Rs176 per share. This reflects a continuation of Indus Motor’s strong dividend track record, though investors had been anticipating stronger earnings growth in line with rising sales volumes.

Net sales climbed significantly during the year. In 4QFY25, revenue rose 28% year-on-year and 15% quarter-on-quarter to Rs69.6 billion. Unit sales surged to 11,775 vehicles in the quarter, up 67% compared to the 7,069 units sold in 4QFY24, and 30% higher than the 9,077 units sold in 3QFY25. This growth in volume reflects a broader recovery in Pakistan’s automobile sector amid improved supply chain conditions and stronger demand.

Other income, primarily derived from cash and short-term investments, declined 6% year-on-year in the quarter but rose 42% sequentially to Rs3.98 billion. For the full fiscal year, other income increased 9% to Rs14.95 billion. The effective tax rate for FY25 stood at 39%, higher than the 35% recorded in FY24, reflecting changes in corporate taxation and government fiscal measures.

An important highlight in the results was the sharp increase in customer advances, which reached Rs34 billion in FY25, marking the highest level in two and a half years. Analysts note that this suggests strong order bookings for upcoming deliveries, offering revenue visibility for the months ahead.

Despite the margin pressures, Indus Motor continues to trade at attractive valuation multiples. Based on forward estimates, the company’s price-to-earnings (P/E) ratio is projected at 6.5x for FY26 and 5.9x for FY27, while dividend yields remain robust at 9–10%.

The company’s performance underlines the recovery trend in Pakistan’s auto industry, where easing import restrictions and increased consumer demand have supported a rebound in volumes. However, pressure on margins due to shifts in consumer preferences and growing competition in the SUV and pickup segments remains a concern for future profitability.

Indus Motor’s FY25 results highlight both opportunities and challenges in the automotive market. While higher sales volumes and improved yearly margins reflect operational resilience, the quarterly weakness in profitability signals that sustaining growth will require careful management of product mix and competition dynamics.

Looking ahead, industry analysts expect the company’s strong balance sheet, steady dividend policy, and rising customer advances to provide a buffer against volatility. The company’s future performance will hinge on maintaining its share in the SUV and pickup segments while leveraging its established Corolla and Yaris models to capture mass-market demand.